As we turn the calendar page to a new year, the financial landscape continues to evolve. If you are a homeowner or a prospective buyer in London, ON, you likely felt the ripples of the economic shifts that defined late 2025. Now, standing at the threshold of 2026, the question on everyone’s mind is: What comes next?

Navigating the mortgage market requires more than just reacting to today’s rates; it requires a strategic roadmap. Whether you are looking to purchase your first home in Hyde Park, renewing a mortgage for your family home in Old South, or considering an investment property near Western University, planning is your strongest asset.

In this comprehensive guide, I, Michael Bonifero, your local London mortgage broker, will walk you through the essential steps to secure your financial future in 2026. We will analyze the 2026 economic outlook, compare rate strategies, and provide a month-by-month plan to ensure you are mortgage-ready.

The 2026 Mortgage Landscape: What Londoners Need to Know

To plan effectively, we must first understand the terrain. As discussed in my previous post, the 2025 Year-End Mortgage Market Recap, the volatility of the past few years has taught us that agility is key. As we move into 2026, several factors are shaping the local market here in London and across Ontario.

1. The Stabilization of Interest Rates

While I cannot predict the future with 100% certainty, market indicators suggest that 2026 may bring a period of stabilization relative to the aggressive hikes and cuts seen in previous years. The Bank of Canada is striving for equilibrium. For borrowers, this means the era of “wait and see” might be transitioning into an era of “act with caution.”

2. The “London Advantage” Remains

Despite price corrections across the province, London, Ontario remains a resilient market. We continue to see migration from the GTA, driven by the search for affordability and lifestyle. This sustained demand impacts housing inventory, meaning that while rates are a major factor, competition for quality homes in neighborhoods like Byron and Lambeth remains a reality for buyers.

3. Regulatory Changes and Qualification

The “Stress Test” remains a hurdle, but new lending products and extended amortization options for specific buyer groups (like first-time buyers purchasing new builds) are creating opportunities. Understanding these nuances is where a professional mortgage broker becomes indispensable.

Strategic Planning for Different Borrower Profiles

A roadmap is useless if it doesn’t lead to your specific destination. Your strategy for 2026 depends heavily on your current position in the property lifecycle.

For the First-Time Home Buyer

If 2026 is the year you plan to buy your first home, your focus must be on affordability and preparation.

- Maximize the FHSA: Ensure you are fully utilizing the First Home Savings Account. The tax-free growth combined with tax-deductible contributions is the most powerful tool in your arsenal.

- Pre-Approval vs. Pre-Qualification: In a competitive London market, a simple pre-qualification isn’t enough. You need a fully vetted pre-approval to be taken seriously by sellers.

- Budget for “Closing Costs”: Many first-time buyers in London forget to budget for Land Transfer Tax (LTT) and legal fees. Remember, London has a municipal LTT but thankfully no additional municipal tax like Toronto.

For the Mortgage Renewer

If your mortgage is up for renewal in 2026, you might be facing a higher rate than you secured in 2021. This is the “payment shock” zone.

- Start Early: Do not wait for your bank’s renewal letter, which usually arrives 30 days before maturity. We should start chatting 4 to 6 months in advance.

- Shop the Market: Lenders count on laziness. They offer a renewal rate hoping you will just sign it. As your broker, I can shop that renewal date across dozens of lenders to ensure you aren’t paying a “loyalty tax.”

- Consider Refinancing: If high-interest consumer debt has piled up, 2026 might be the year to refinance at renewal, consolidating that debt into your mortgage to lower overall monthly cash flow obligations.

For the Real Estate Investor

London is a hub for student rentals and multi-family units. For investors, 2026 is about cash flow management.

- Review Rental Income: Ensure your leases reflect current market rates to offset higher borrowing costs.

- Leverage Equity: If you have built significant equity in your primary residence, we can discuss a HELOC (Home Equity Line of Credit) to act as a war chest for purchasing investment opportunities that arise in 2026.

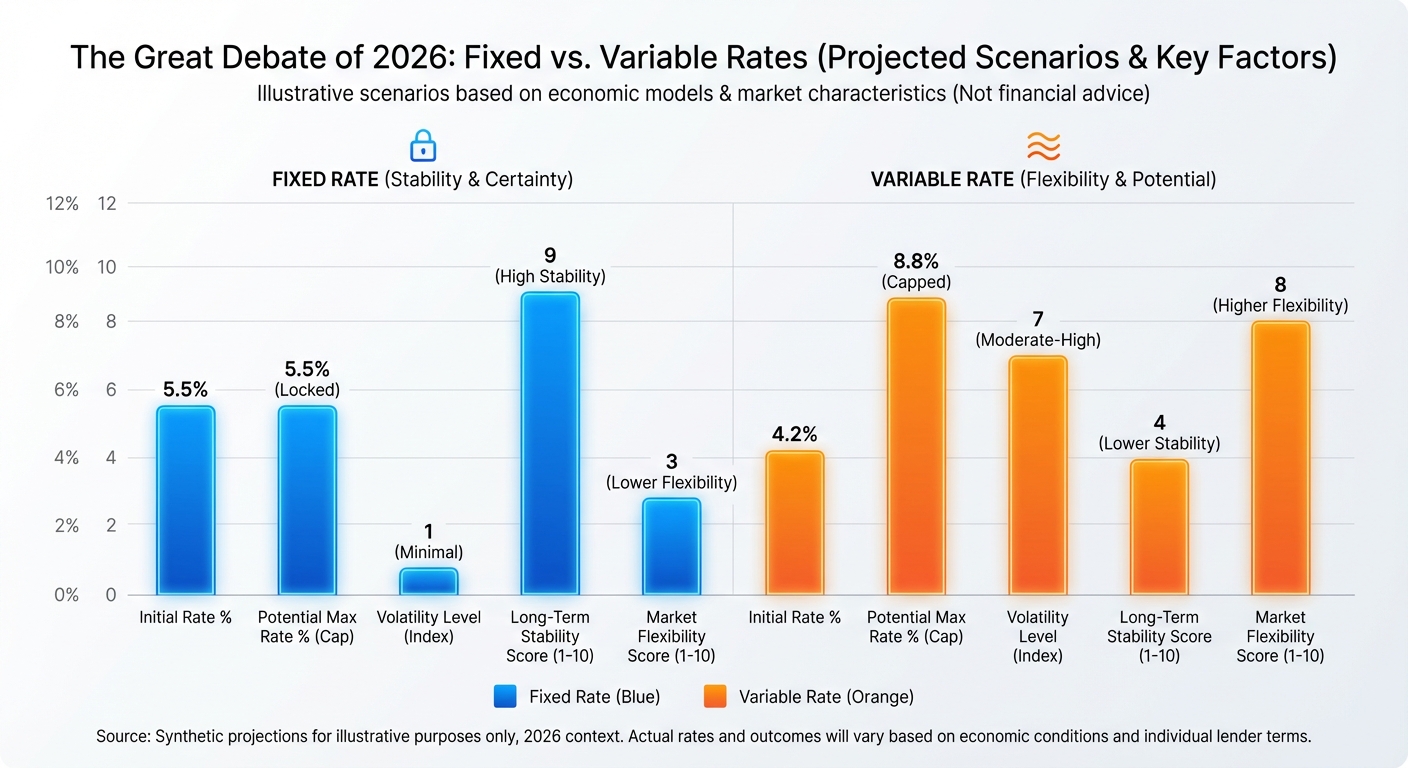

The Great Debate of 2026: Fixed vs. Variable Rates

One of the most common questions I receive at my office is: “Mike, should I go fixed or variable?” The answer in 2026 is nuanced. Let’s break down the current thinking.

| Rate Type | Pros in the 2026 Market | Cons in the 2026 Market | Ideal Borrower Profile |

|---|---|---|---|

| Fixed Rate |

|

| First-time buyers, those on a fixed income, or anyone who loses sleep over market news. |

| Variable Rate |

|

| Experienced investors, borrowers with high disposable income, or those planning to sell/move soon. |

Note: The table above is a general guide. Your specific situation requires a personalized consultation. Contact me today to run the numbers for your scenario.

Your 2026 Mortgage Roadmap: A Month-by-Month Guide

Success is in the schedule. Here is a suggested timeline to keep your mortgage goals on track this year.

Q1: Assessment and Cleanup (January – March)

January: Pull your credit report. Check for errors. In Canada, your credit score is the gatekeeper to the best rates. If you find discrepancies, dispute them now.

February: Gather your documents. T4s, Notices of Assessment (NOAs), and Letter of Employment. Having these digital and ready prevents scrambling later.

March: The “Spring Market” in London usually heats up. If you are buying, get your pre-approval locked in now to hold a rate for 90-120 days.

Q2: Execution and Hunting (April – June)

April: For buyers, this is house-hunting season. For renewers, if your maturity date is in the fall, we start looking at rates now.

May: Review your budget. Has inflation impacted your grocery or utility bills? Adjust your maximum mortgage qualification number based on real life, not just what the bank says you qualify for.

June: Mid-year check-in. If you have a variable rate mortgage, let’s review your trigger rate and amortization schedule.

Q3 & Q4: Review and Planning for 2027 (July – December)

Why Choose a Local London Broker in 2026?

In a digital age, you can get a mortgage from a call center in Toronto or an algorithm on a website. However, Real Estate is inherently local. As a specialized London Mortgage Broker, I offer insights that algorithms cannot.

- Local Appraisers: I know which lenders use appraisers that understand the value of a renovated century home in Woodfield versus a new build in Talbot Village.

- Local Lawyer Connections: I work daily with real estate lawyers in London, ON, ensuring your closing process is smooth and on time.

- Access to Non-Bank Lenders: If the “Big 5” banks say no, I have access to credit unions, monoline lenders, and private funds that focus on the London area.

Frequently Asked Questions (FAQs)

1. What are the predicted mortgage rates for London, ON in 2026?

While specific rates change daily, the consensus for 2026 is a stabilizing market. We do not anticipate the rock-bottom rates of 2020, but we also hope to see relief from the peaks of 2024. For the most current rate sheet, please email me directly.

2. How far in advance should I start planning my mortgage renewal?

I recommend starting the conversation 4 to 6 months before your maturity date. This allows us to lock in a rate early. If rates drop before you renew, we can usually float down to the lower rate. If rates rise, you are protected.

3. Can I buy a home in London with less than a 20% down payment?

Yes. If the home price is under $1 million, you can purchase with as little as 5% down (on the first $500k) and 10% on the remainder. This requires mortgage default insurance (CMHC/Sagen). We can calculate exactly what your down payment needs to be.

4. Is it better to use a Mortgage Broker or go to my bank?

Your bank can only offer you their specific products. As a broker, I have access to dozens of lenders, including major banks, credit unions, and trust companies. This means I negotiate on your behalf to find the best rate and terms for you, not the bank’s shareholders.

5. Does getting a pre-approval hurt my credit score?

A pre-approval requires a “hard check” on your credit, which can temporarily lower your score by a few points. However, this is negligible compared to the power of being a verified buyer. Furthermore, multiple checks from mortgage inquiries within a short window (usually 14-45 days) often count as a single inquiry for scoring purposes.

Ready to Map Out Your 2026 Mortgage Strategy?

The road to homeownership or a successful renewal doesn’t have to be a solo journey. In 2026, align yourself with a professional who understands the local London market and puts your interests first.

Whether you are ready to apply or just have a few questions about where rates are heading, I am here to help. Let’s build a plan that fits your budget and your lifestyle.

Contact Mike Bonifero Today

Phone: 519-851-459

Email: Mike@boniferromortgages.ca

Click Here to Start Your Application